Get in Touch

Email Us

info@smartlogics.inReach Out

+91-9760730500Find Us

Corporate Office

420, NH 58, Gayatri Garden Partapur Bypass,

Meerut, Uttar Pradesh, 250002 (India)

Best GST Billing Software for Small & Medium Business

Start using our billing software which comes with best in class smart features to help your business grow.

Work Smart, rather than Work Hard !

Some Silent Features

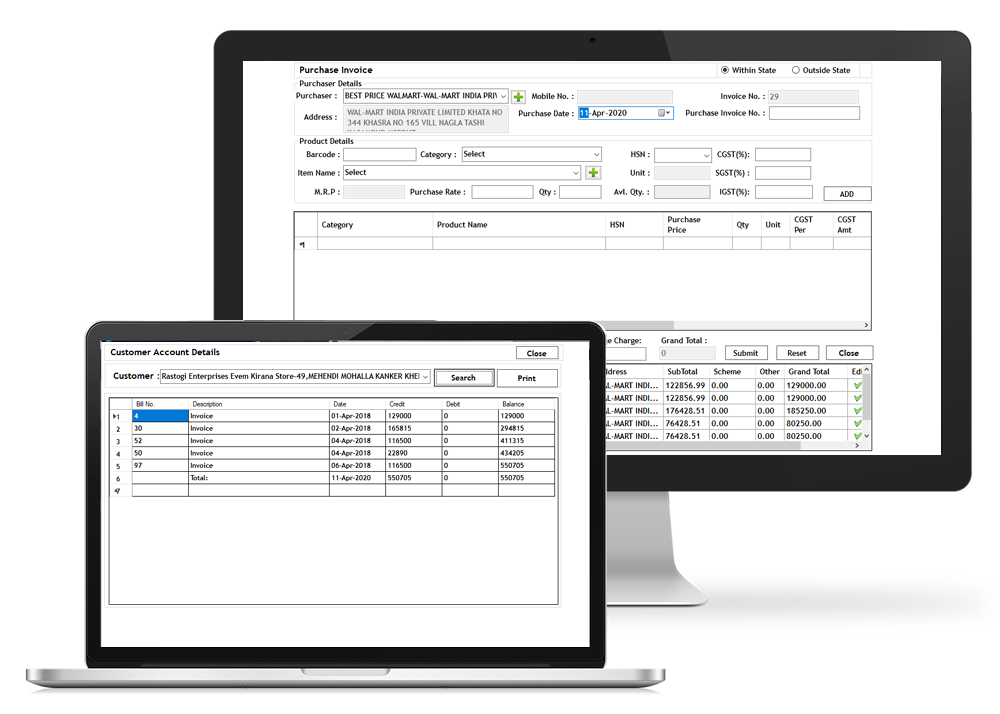

Our all Invoices are beautifully designed as per the customer Requirement & compliant with GST rules and regulations.

With our GST Billing Software you can easily create unlimited products & manage all stock with one click.

Create GST compliant Quotation & Performa Invoice with our extremely easy interface.

Create credit & debit notes against any invoice With accurate templates and professional design.

Record & track payments for invoices created in the system & take print out with one click

Log & keep track of your petty cash expenses with custom created categories as per your business.

Our Billing Software allows you to create unlimited purchase orders that you can easily turn to bills as needed.

Either it is Including Tax or Excluding Tax for your product, GST Billing Software will do all the detailed calculations of SGST, CGST or IGST automatically.

Send you Invoice, Quotation or any other document on email, SMS in just few clicks.

Smart GST Billing Software offer you advance customization as per the client business. From calculation, formatting, or printing everything is customized.

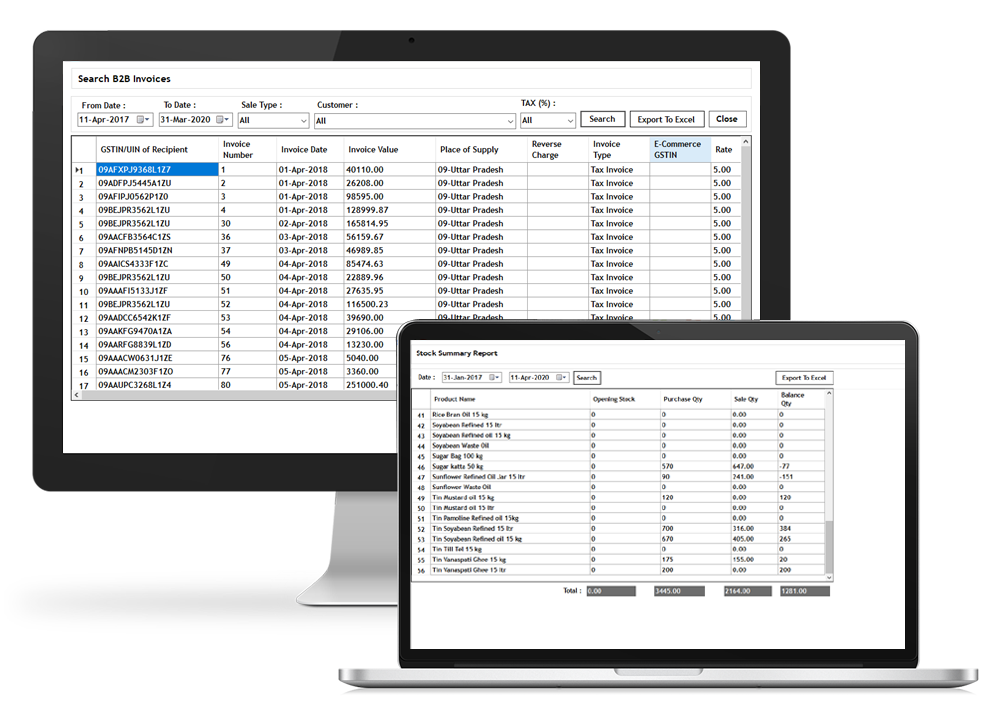

Smart GST Billing Software contains all your GST billing reports from invoices to purchase orders, GSTR 1, GSTR 3B & much more.

All your data is safely stored and secured on your PC. The backup and restore feature helps to protect your invoicing database form unfortunate events or to transfer it from one PC to another.

You can easily export your data like customer, product & invoice to excel sheet with one click.

Our excellent support team will help you to resolve any query related to our software.

More than 1400+ Business are using Smart GST Billing Software

Fastest growing GST Billing Software in India

Let's build an

amazing project

Drop Us A Line

Why Choose SMART Logics?

14+ Year

Experience

Committed

to Quality

We’re

Affordable

Customize to

your Needs

Unconditional

Support

Satisfaction

Guaranteed

One Stop

Services

Dedicated

developers

Handle Tight

Deadlines

Let's Get Started Now!

Please fill out the quick form and we will be in touch with you at lightning speed.

SERVICES

PRODUCTS

COMPANY

Connect

SMARTLOGICS SERVICES PRIVATE LIMITED

Support

© Smartlogics Services Pvt. Ltd., 2024. All Rights Reserved.